![How Can NBFCs Use an AI System for Loan Pre-Qualification [2026]](/content/images/size/w2000/2026/06/How-Can-NBFCs-Use-an-AI-System-for-Loan-Pre-Qualification.jpg)

When a borrower walks into a bank branch or speaks to a Direct Sales Agent (DSA), they rarely expect an instant loan approval. What they do expect is clarity.

- "Am I likely to qualify?"

- "What documents will I need?"

- "How much could I be eligible to borrow?"

For many banks and NBFCs, answering these questions takes days. Frontline teams often need to wait for underwriting or credit teams to interpret lending policies before they can provide reliable guidance.

In this workflow, generic AI can't be used as it is designed to make autonomous guesses. Whereas all lending needs strict compliance.

To safely automate loan pre-qualification, AI must focus on credit decision support. It must bridge the gap between compliance and sales. It must help frontline sales team/DSA agents successfully translate complex policies into real-time, actionable insights and next-steps.

One way these AI systems achieve this is through soft signals (early indicators) that estimate whether a borrower is likely to qualify before a formal underwriting process begins. Used responsibly, soft signals help improve borrower experience without changing credit policies or bypassing human oversight.

In this article, you'll learn how AI systems can support loan pre-qualification and how banks and NBFCs can bring AI guidance to their sales floor while maintaining governance, compliance, and human accountability.

WHAT YOU'LL LEARN:

- What Is the Hidden Cost of Delayed Credit Answers?

- How Can DSAs Use AI-Powered Loan Pre-Qualification?

- Decision-Making vs. Decision Support: What's the Difference?

- How Does the Pre-Qualification Soft Signal AI System Work?

- How Can NBFCs Safely Deploy AI in Loan Pre-Qualification?

- How Gyde Helps BFSIs and NBFCs Implement AI in Loan Pre-Qualification?

- Frequently Asked Questions (FAQs)

What Is the Hidden Cost of Delayed Credit Answers?

Every loan application begins with a conversation. A borrower meets a branch representative or Direct Sales Agent (DSA), explains their financing needs, shares details such as income, employment, existing obligations, and available documents, and asks a simple question:

"Am I likely to qualify for this loan?"

Providing an early indication of eligibility before a formal underwriting review is known as loan pre-qualification. Traditionally, final credit eligibility decisions sit with the credit team, which creates a back-and-forth that causes delays. There's no way for DSA teams to reliably answer borrower questions during the first interaction.

Most loan pre-qualification processes struggle because:

- Customer information is incomplete or spread across multiple systems.

- Credit policies are detailed, frequently updated, and difficult for frontline teams to interpret consistently.

- Borrowers wait longer for clarity, creating uncertainty during a critical stage of the lending journey.

The impact is felt across the business. Delayed credit guidance leads to abandoned applications, lower conversion rates, longer sales cycles, and a poorer customer experience. Every additional handoff between sales and credit increases the likelihood that a borrower loses interest or chooses another lender.

This is precisely the gap AI-powered loan pre-qualification is designed to address. It does not make lending decisions automatically. But, it does give frontline teams timely, policy-guided eligibility insights while keeping final credit decisions with underwriters.

How Can DSAs Use AI-Powered Loan Pre-Qualification?

DSAs can use AI-powered credit decision support to:

- Check borrower eligibility instantly based on income, credit profile, obligations, and loan requirements.

- Answer customer questions faster using policy-based guidance during conversations.

- Identify missing documents or information before submitting applications.

- Recommend the next best action, such as additional documents, co-applicants, or suitable loan products.

- Reduce application rejections and rework by submitting higher-quality loan files.

- Improve conversion rates by giving borrowers immediate eligibility insights.

However, financial institutions cannot simply deploy a generic AI model and allow it to advise DSAs. Lending decisions operate within strict policy, risk, and compliance frameworks. Uncontrolled AI outputs can create governance gaps, inconsistent guidance, and regulatory concerns.

Effective credit decision support systems therefore act as guardrailed intelligence, where AI operates within:

- Approved lending policies and eligibility criteria.

- Product-specific credit rules.

- Compliance and audit requirements.

- Human review and underwriting oversight.

- Clear accountability for final decisions.

This Mid-Size NBFC leadership did not need an AI agent that approved or rejected applicants. It needed a system that could surface a reliable credit signal while leaving accountability with humans.

In other words, the goal was not decision-making. It was decision support.

Decision-Making vs. Decision Support: What's the Difference?

- While the difference between an AI that makes decisions and one that supports them sounds like a subtle distinction, in financial services, it is everything.

- It is quite literally the boundary between a tool a risk team will champion and one they will completely block.

- A DSA’s job is to source, build trust, and close the deal—not to do the underwriter’s work.

- The system's role is simply to transfer institutional policy down to the frontline, instantly translating raw borrower data into actionable next steps.

Decision-making vs Decision Support

| Decision-Making | Decision Support | What Gyde Does | |

|---|---|---|---|

| Outcome | System produces approved, declined, or referred outcomes. | Human receives structured information to act on. | Surfaces policy-grounded reasoning for the human to judge. |

| Accountability | Model made the call, human signed off. | Human owns the decision and the reasoning behind it. | Accountability remains with the human by design. |

| Regulator Question | Can the model's reasoning be reproduced or explained? | Can the human explain the decision they made? | Consistent, auditable reasoning is surfaced every time. |

| Customer Challenge | Why did the system decline me? | Why did the officer decline me? | The officer can explain the outcome because they made the call. |

| Risk | Diffused accountability and difficult audits. | Inconsistent input quality without the right system. | Consistency without removing human judgment. |

How Does the Pre-Qualification Soft Signal AI System Work?

Step 1: The Agent Starts the Chat

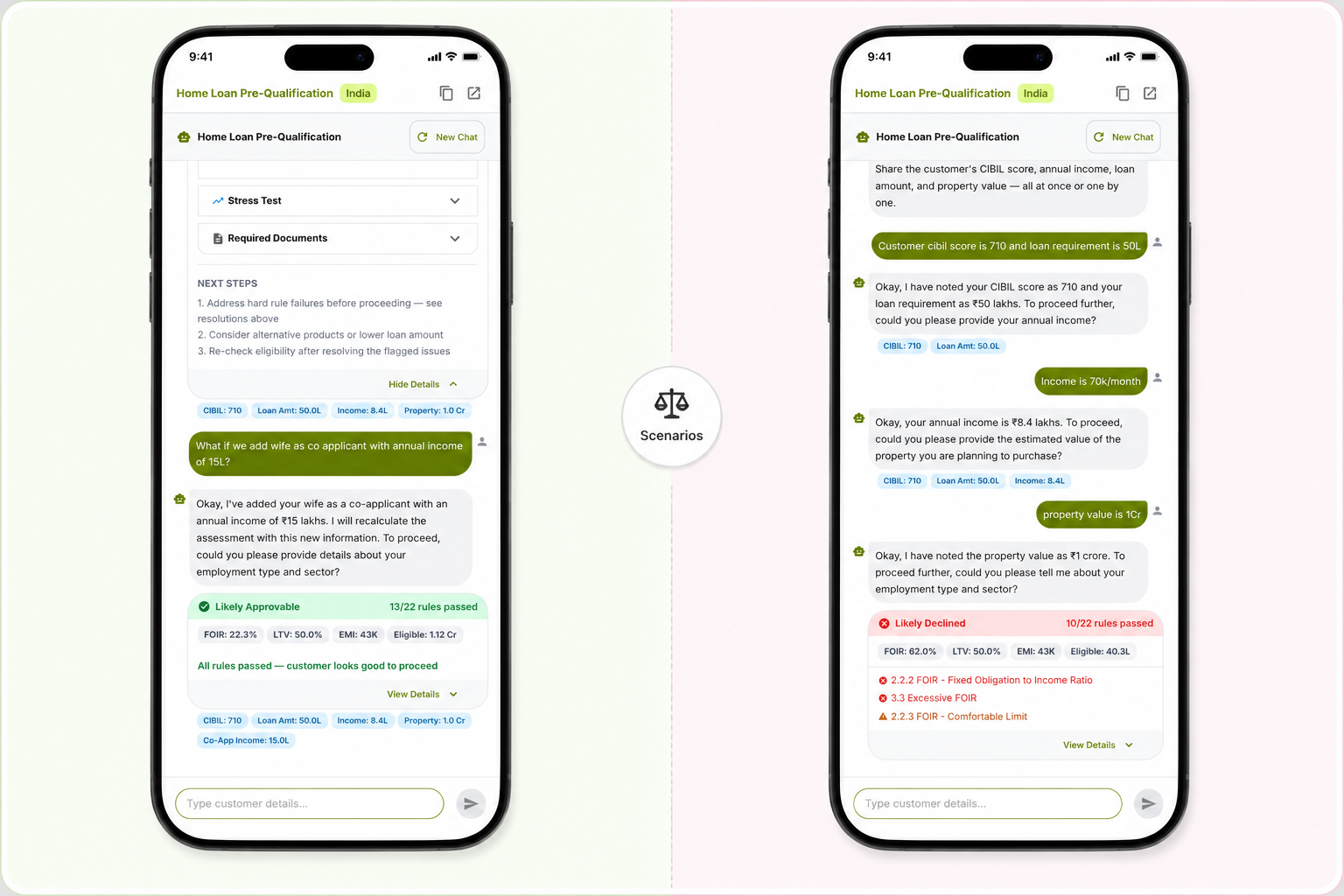

Right there in the customer meeting, the agent opens Gyde and enters fixed variables the customer can answer in seconds. CIBIL score, loan amount, income, property value are specific fields that need to be completed getting filled in behind the scenes, pulled out of plain language one at a time.

Step 2: An Instant Read Appears

In seconds, a soft-signal card comes back. It shows a clear status (likely approvable, needs a closer look, or not a fit yet) along with the maximum eligible loan amount, the key affordability ratio (FOIR), the loan-to-value figure (LTV), and the exact documents to collect. The customer can see, in that meeting, roughly where they stand.

Step 3: The Conversation Deepens

If the customer wants to go further, the agent adds more detail: employment type, existing EMIs and liabilities, preferred tenure, co-applicant income. Each additional input sharpens the read. By the end of the meeting, the agent has a materially complete picture.

Step 4: The File Gets Stress-Tested

Before anything moves forward, the system tests how the file holds up under pressure. What if rates rise 2%? What does a shorter 15-year tenure do to monthly obligations? These are the questions the credit desk will ask anyway. The system surfaces them early, so nobody is surprised later.

Step 5: A Full Signal Report for the Underwriter

One tap converts the conversation into a structured credit decision signal report. It contains:

- The eligibility calculation, laid out in full

- Every policy rule, with a clear pass or flag

- Compensating strengths weighed in

- Stress-test results

- A recommendation with conditions

- A plain-language version for the customer

The underwriter gets a file that has already been pre-structured. They don't start from scratch. They start from a documented, policy-aligned read and apply judgment to the parts that actually need it.

As shown in the image, when a DSA inputs the initial borrower details, the AI system displays a soft signal of Likely Declined.

However, once a co-applicant is added (since loan eligibility is calculated using both people's details) the AI system re-runs the same rules against the new numbers. It instantly updates its soft signal to match the revised data, shifting to Likely Approvable.

If the verdict shifts the right way and the new numbers hold together, that's real evidence the logic underneath is sound and not just that it gave one plausible-sounding answer once.

How Can NBFCs Safely Deploy AI in Loan Pre-Qualification?

Deploying AI in loan pre-qualification isn't about replacing underwriters with automated decisions. It's about introducing AI into the lending workflow in a controlled, governed manner that improves frontline productivity while preserving credit discipline.

A safe AI Implementation plan typically follows four key principles:

1. Align AI with Existing Credit Policies

Before AI is made available to frontline teams, it should be configured using the institution's existing lending policies, product rules, and eligibility criteria. Validating the AI against historical loan decisions helps ensure its recommendations align with established credit practices before customer-facing use.

2. Begin with a Controlled Pilot

Rather than deploying AI across the entire organization, start with a limited group of branch representatives and Direct Sales Agents (DSAs). This allows business and credit teams to evaluate usability, identify policy gaps, and gather operational feedback before scaling.

3. Keep Humans in the Decision Loop

During deployment, AI should function as a decision support system. Frontline teams can use AI-generated soft signals to guide borrower conversations, while credit teams continue making all final eligibility and approval decisions. Comparing AI recommendations with actual underwriting outcomes helps establish trust and measure accuracy without increasing lending risk.

4. Scale Based on Validated Results

Once business, credit, and compliance teams confirm that the AI consistently aligns with lending policies and delivers measurable operational improvements, the deployment can be expanded across additional branches, products, or DSA networks.

This approach reduces two of the biggest risks associated with enterprise AI deployment:

- Allowing AI to influence lending decisions before its outputs have been validated.

- Scaling AI across the organization before there is sufficient evidence that it performs consistently within policy and governance requirements.

Impact Seen By a Mid-Size NBFC Customer

After deploying AI-assisted loan pre-qualification, the institution reduced manual effort, improved borrower experience, and enabled sales teams to focus on applications with a higher likelihood of approval.

How Gyde Helps BFSIs and NBFCs Implement AI in Loan Pre-Qualification?

Gyde works as an AI transformation partner for financial institutions, helping lending teams move from AI experimentation to production deployment.

Rather than delivering a standalone AI application, Gyde combines people, platforms, and implementation expertise to build Specific Intelligence Systems tailored to lending operations.

Ready-to-Use AI Solutions

Production-ready AI applications help teams improve borrower qualification, sales conversations, underwriting support, and operational workflows without lengthy development cycles.

Embedded Intelligence POD

A dedicated POD team works alongside business, credit, and operations teams to configure workflows, refine knowledge, and support implementation from pilot to production.

Curated Model and Tool Stack

The underlying models, frameworks, and tools are selected and optimized for the specific lending use case, allowing institutions to focus on business outcomes rather than technology decisions.

From One Use Case to Enterprise Intelligence

What begins as a pre-qualification system can expand into adjacent workflows such as document verification, underwriting support, collections, and portfolio servicing, creating a connected intelligence layer across lending operations.

FAQs

1. What is the difference between loan pre-qualification and loan pre-approval?

Loan pre-qualification provides an initial estimate of a borrower's eligibility based on self-reported financial information, while pre-approval involves a deeper verification of income, credit history, and supporting documents. Pre-qualification is typically faster and helps lenders identify promising applicants earlier in the funnel.

2. How does AI improve loan origination efficiency for NBFCs?

AI accelerates loan origination by automating data collection, eligibility assessments, document verification, and borrower screening. This reduces manual effort, shortens turnaround times, and allows sales teams to engage qualified prospects more effectively.

3. How do NBFCs ensure AI-driven credit assessment remains compliant with regulations?

NBFCs typically deploy AI systems that provide recommendations rather than autonomous lending decisions. Human underwriters retain final authority, while audit trails, explainable outputs, and policy-based workflows help maintain regulatory compliance.

4. What role does credit scoring play in AI-powered lending?

Credit scoring serves as one of several inputs used by AI models to assess risk. Modern lending systems often combine credit bureau data with income analysis, debt obligations, repayment behavior, and policy rules to generate a more comprehensive evaluation.

5. Can AI help Direct Selling Agents (DSAs) increase loan conversion rates?

Yes. AI equips DSAs with real-time eligibility insights, recommended next actions, and document requirements, helping them focus on qualified prospects and reduce time spent on applications unlikely to proceed.